The semiconductor industry rarely shifts materials without a compelling structural trigger. Glass core substrates are emerging not simply because they are “better,” but because system-level demands from AI, high-performance computing (HPC), and chiplet architectures are forcing a rethink of packaging foundations.

What we are witnessing is not just material innovation; it is the early formation of a new packaging economy.

A Demand-driven Inflection Point in Advanced Packaging Evolution

The future of advanced semiconductors isn’t just about miniaturization; it’s about packaging innovation. The transition towards novel packaging approaches is being shaped by the rising demand for Artificial Intelligence (AI) and High Performance Computing (HPC). As compute architectures evolve to be chiplet-based and heterogeneously integrated, the substrate is becoming the determining factor for architecture’s success.

Currently, glass core substrates are entering this landscape at a critical inflection point.

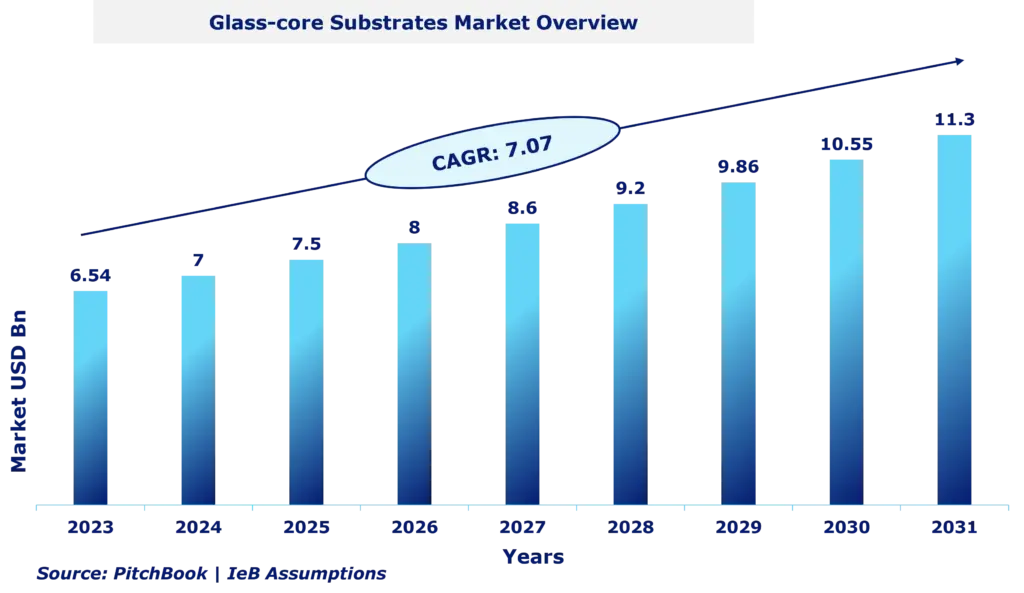

The current state of the market is still in the early stages of commercialization. However, the market growth anticipation is positive over the decade, driven less by incremental adoption and more by structural demand shifts.

AI accelerators, data center CPUs/GPUs, and next-generation networking infrastructure are pushing packaging technologies to deliver higher interconnect density, lower signal loss, and improved thermal stability, requirements that conventional organic substrates struggle to meet at scale.

Let’s understand the key reasons behind this momentum in the advanced semiconductor packaging:

- AI workloads demanding ultra-high bandwidth and low latency

- HPC systems requiring large package sizes with minimal warpage

- Packaging innovations (2.5D, 3D, chiplets) outpacing substrate capabilities

This is not a supply-led transition; it’s actually the demand-driven shift.

Current Market Trends Reshaping the Glass Core Substrate Landscape

There are several trends driving growth & development within the glass core substrate market. Four of the major areas of development include:

AI-led Acceleration of Substrate Innovation

AI is not just increasing compute demand; it is reshaping packaging priorities. Signal integrity will become increasingly important as systems move beyond 100 GHz. Therefore, substrate materials are now playing a role in how well a system performs. Because glass has significantly less electrical drain than traditional substrate materials. Hence, glass is likely to be considered a crucial raw material for high-performance systems, instead of simply a premium product.

Shift Toward Panel-level Packaging

The ability to process large-area panels using glass substrates is enabling manufacturers to achieve higher levels of throughput and lower costs at scale. This may lead to the adoption of panel-level packaging (PLP), especially for large form-factor AI packages.

Emergence of Hybrid Material Ecosystems

Rather than transitioning to single material or technology; the industry is exploring hybrid solutions such as glass-organic and glass-ceramic cores, which address the trade-offs associated with cost, manufacturing feasibility, and performance. While this represents a transitional period in terms of material selection rather than a transition from one material to another, it also represents a significant paradigm shift for the industry.

From R&D to Pilot-Line Race

This is a notable trend occurring in the substrate industry. Companies are shifting their focus from validating their technologies in research and development labs to scaling those same technologies into production. Rather than competing solely over who has developed the feasible technology, the competitive advantage is rapidly becoming who can first develop a commercially viable version of that technology.

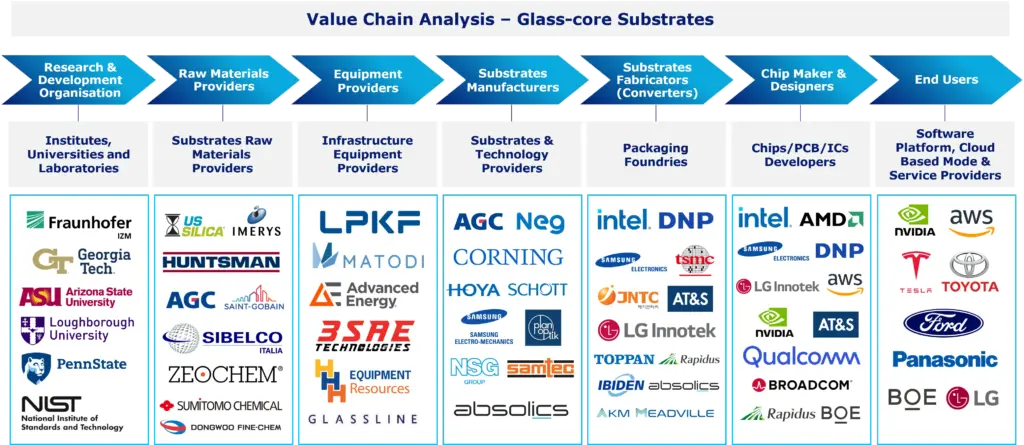

Value Chain Analysis: Decoding the Multi-layered Ecosystem Behind Glass Core Substrate Adoption

The glass-core substrate ecosystem is not a linear chain; it’s a multi-layered value network structured across 7 distinct segments, grouped into four broader tiers: Upstream, Midstream, Core Substrate, and Downstream. Each segment plays a specialized role, but the real dynamic lies in how tightly they are interlinked.

Upstream: Research & Raw Material Foundation

The upstream value chain consists of organizations that advance innovation related to glass substrates. Two groups of organizations drive innovation in this space:

Research & Development Organizations

This includes organizations, such as Fraunhofer-Gesellschaft, Georgia Institute of Technology, and Arizona State University. Research in this space provides the fundamental knowledge required to create innovative glass substrate compositions and architectures that enhance thermal properties and improve signal quality.

Raw Materials Providers

Material suppliers such as AGC Inc., Corning Incorporated, SCHOTT AG, Nippon Electric Glass, along with chemical companies like Huntsman Corporation and Sumitomo Chemical, provide the initial raw materials used to fabricate glass substrates.

Midstream: Equipment & Infrastructure Enablement

The midstream value chain consists of enterprises that apply research findings & raw materials to create products and services that are critical to the successful application of glass substrate technology. Two groups of companies exist in this space:

Infrastructure Equipment Providers

This segment covers companies that provide equipment and/or infrastructure necessary to manufacture glass substrates. Organizations in this space include Applied Materials, KLA Corporation, LPKF Laser & Electronics, and ERS Electronic. The primary function of organizations in this space is to develop processes and provide tools necessary to create unique features of glass substrates, such as Through-Glass Via (TGV) formation and precise lithography.

Substrate Technology Providers

Firms such as Corning Incorporated, HOYA Corporation, SCHOTT AG, and AGC Inc. extend beyond raw materials into engineered substrate solutions.

Core: Substrate Manufacturing

At the heart of the value chain are substrate manufacturers who translate materials and processes into functional packaging platforms.

Substrate Manufacturers

This is the central execution layer, where companies like Absolics, Plan Optik AG, Samsung Electronics, and LG Innotek convert material and process innovations into manufacturable substrates.

Downstream: Fabrication, Design & End-Use

The downstream value chain represents companies involved in the final stages of product delivery. The primary functions of organizations in this space include:

Substrate Fabricators & Chip Designers

This segment includes advanced packaging players and chip designers such as Intel, Taiwan Semiconductor Manufacturing Company, Samsung Electronics, Advanced Micro Devices, Qualcomm, and NVIDIA. They integrate glass substrates into advanced packaging architectures such as 2.5D/3D and chiplet-based systems.

End Users & Platform Providers

End-market demand is driven by companies such as Amazon Web Services, Tesla Inc., Ford Motor Company, Panasonic Holdings, BOE Technology Group, and LG Electronics.

Commercial Adoption of Glass Core Substrates

The next few years represent a period of transition from research-focused activities to early commercial production line activities. During this timeframe, companies are transitioning from laboratory-scale testing to larger-scale production. This represents a major milestone in the commercialization of glass-core substrates. As a result of this transition, companies will begin to make significant investments in commercial-scale manufacturing operations.

Several companies are planning to invest heavily in developing commercial-scale operations for producing glass-core substrates. Many of these companies believe they will be able to benefit from economies-of-scale once they reach a certain threshold of commercial-scale production.

Recent government policies aimed at promoting domestic semiconductor industries are expected to increase competition among foreign companies seeking entry into global markets dominated by established players. For example, the U.S. government recently implemented policy initiatives aimed at encouraging American companies to pursue independent strategies to address the global shortage of semiconductors. Similarly, similar initiatives have been introduced by governments in Japan, South Korea, and China.

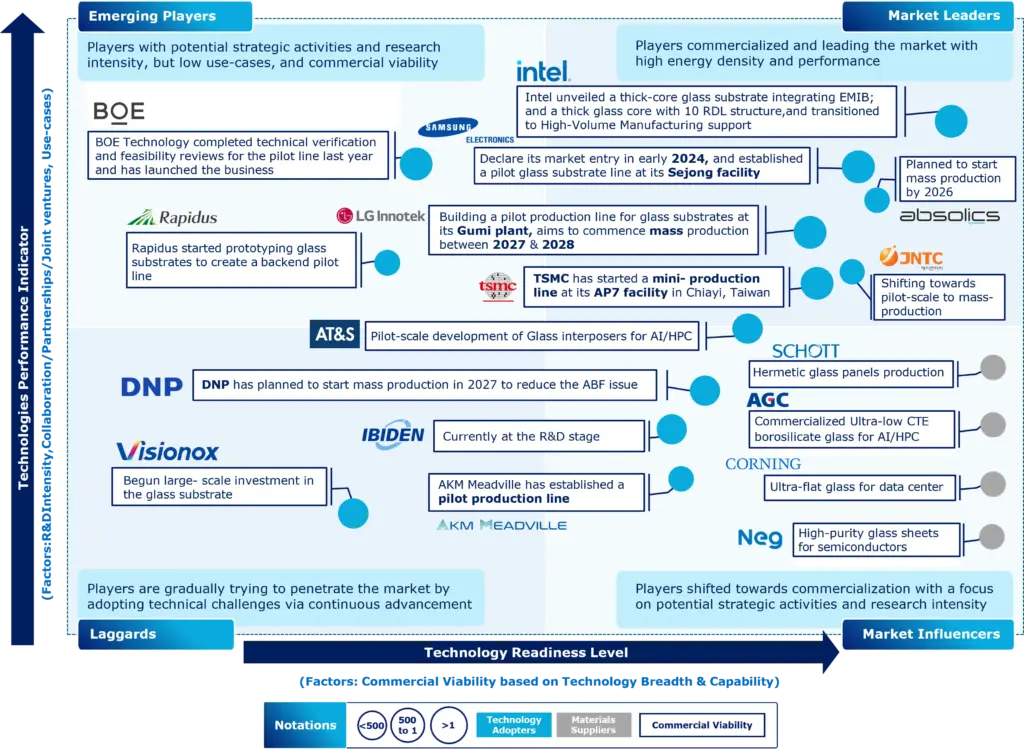

From Validation to Scale: Tracking the Glass Core Substrate Adoption Curve

The adoption of glass-core substrates is progressing as a staged, industry-driven transition, shaped by how quickly leading players can translate material innovation into scalable manufacturing.

Between 2023 and 2025, the focus has been on validation and ecosystem alignment. Intel demonstrated the feasibility of integrating AI accelerators and HPC systems, highlighting gains in interconnect density and reduced warpage. In parallel, Samsung Electronics advanced pilot lines for multi-chip and high-bandwidth packaging, while LG, Innotek, and Absolics built early infrastructure targeting AI, RF, and photonics applications. Ecosystem players like Japan Electronic Materials Corporation (JNTC) further supported validation through cross-industry partnerships.

At this stage, the emphasis has been on proving capability, not scaling volume.

Looking ahead to 2026–2028, the industry is expected to transition into pilot production and early commercialization, where yield and process maturity become critical. Intel is anticipated to move toward production readiness around 2026, while Samsung Electronics is targeting a ramp-up closer to 2027 for high-density AI packaging. Substrate players such as TOPPAN Holdings, AT&S, and JCET Group are strengthening capabilities to integrate glass into advanced packaging flows. However, timelines remain uneven. LG Innotek, for instance, is expected to commercialize closer to 2028, highlighting that yield maturity, not intent, dictates adoption speed.

Beyond 2028, the focus is likely to shift toward scaling and broader penetration. Absolics is positioned to support panel-level manufacturing for AI and data center applications, while Intel and Samsung Electronics are expected to expand integration into mainstream advanced packaging. Material suppliers such as AGC Inc. and TOPPAN Holdings will play a key role in scaling supply, enabling expansion into automotive electronics, photonics, and RF systems.

Despite strong momentum, adoption will remain selective rather than universal. Glass-core substrates are expected to dominate performance-critical segments like AI and HPC, while organic substrates continue to serve cost-sensitive markets. This results in a hybrid industry structure rather than full material replacement.

Key Players and Their Recent Activities Driving the Industry

The last 12–18 months mark a clear shift from exploration to execution, with leading players moving beyond evaluation into capacity building, partnerships, and ecosystem alignment.

A defining move came from Intel, which announced its glass substrate platform for advanced packaging, targeting launch readiness between 2026 and 2030. Its demonstrations, particularly EMIB-integrated glass substrates for AI and data center architectures, signal that glass is being positioned at the heart of next-generation chip design, not at the periphery.

At the same time, Samsung Electro-Mechanics is accelerating industrialization, with plans to establish pilot production lines by 2025 and mass production by 2026 for high-end system-in-package (SiP) applications. Its collaboration with Sumitomo Chemical and Dongwoo Fine-Chem to secure glass core materials highlights a broader trend: material supply is becoming a strategic lever, not just an input.

On the materials front, consolidation is already underway. SCHOTT AG strengthened its semiconductor capabilities through the acquisition of QSIL’s quartz business, reinforcing its position in advanced material solutions for AI-driven chip manufacturing. This reflects a growing need for specialized glass formulations tailored to high-performance packaging.

Parallel to this, ecosystem-level collaborations are intensifying. LPKF Laser & Electronics, in partnership with Fraunhofer-Gesellschaft and a consortium of industry players, launched the Glass Panel Technology Group (GPTG). The initiative focuses on scaling panel-level glass substrates for advanced packaging, while advancing laser-based TGV formation; one of the most critical process bottlenecks.

IeB Perspective

Glass-core substrates are transitioning from a promising material innovation to a strategic battleground in semiconductor packaging.

The winners in this space will not be defined solely by material performance, but by:

- Ability to scale manufacturing with viable yields

- Integration across the value chain

- Alignment with AI-driven system requirements

For businesses operating across the semiconductor ecosystem, the question is no longer if glass will play a role. But where in the value chain do you capture value?

If you are evaluating opportunities in advanced packaging, assessing supplier landscapes, or identifying whitespace in the glass-core ecosystem, our team works closely with industry stakeholders to translate these shifts into actionable strategies.

Connect with our experts to explore how glass-core substrates could reshape your roadmap. Fill out the form below to get started.