The global transition toward electrification is reshaping supply chains at an unprecedented pace. While much of the focus has been on battery manufacturing and raw materials sourcing, the need to maintain uninterrupted battery supply across global markets is equally important. This scenario unlocks new business avenues around the storage and management of lithium-ion batteries across global markets.

Unlike conventional industrial products, lithium-ion batteries are classified as Hazard Class 9 dangerous goods. Thus, there must be very strict international transportation regulations, specialized packaging standards, and dedicated handling procedures to safely transport batteries across countries. With increasing demand for batteries within electric vehicles (EVs), battery energy storage systems (BESS), and consumer electronic devices, logistics is evolving from a supporting function into a strategic enabler of the energy transition.

Rising Battery Demand is Creating New Logistics Opportunities

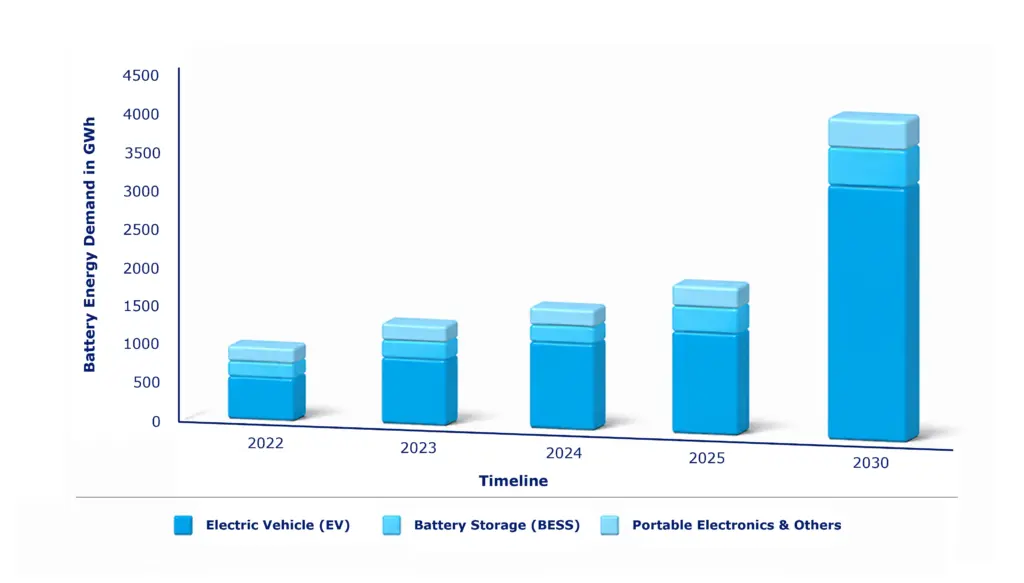

Global battery demand is expected to expand significantly over the coming decade, growing from roughly 1,260 GWh in 2024 to nearly 3,900 GWh by 2030. Electric vehicles account for the largest share of this demand at around 79%. Battery energy storage systems (BESS) represent ~10% and are projected to be the fastest-growing segment as renewable energy deployment accelerates worldwide. Other applications, represented by portable electronics, represent the rest of this demand.

To meet this scale of battery demand, the global lithium requirement is expected to grow from roughly 1.3 million tonnes of lithium carbonate equivalent (LCE) in 2024 to more than 3.6 million tonnes by 2040. Some projections suggest that lithium demand could exceed 5.2 million tonnes, depending on a number of factors, including changes in battery chemistries and the speed at which energy storage solutions gain traction in the marketplace.

This rapid expansion creates many opportunities across transportation, warehousing, inventory management and services associated with the full life cycle of batteries.

Global Manufacturing Concentration is Shaping Battery Logistics

The global lithium-ion battery industry remains highly concentrated, with China accounting for over 70% of worldwide cell manufacturing capacity. While Europe and North America continue to invest in domestic gigafactories, local production remains insufficient to meet rapidly growing demand for electric vehicles (EVs), battery energy storage systems (BESS), and other industrial applications.

As a result, battery supply chains remain deeply interconnected. Large volumes of battery cells, modules, and packs continue to move across continents before reaching automotive manufacturers, energy storage projects, and downstream assembly facilities. This manufacturing concentration has elevated international logistics from a supporting activity to a strategic component of global battery supply chains, requiring specialized transportation networks capable of safely moving hazardous goods across multiple jurisdictions.

What Makes Battery Shipping So Different From Shipping Anything Else?

The transportation of lithium-ion batteries involves far greater complexity than traditional freight.

Battery shipments must comply with stringent regulations, including UN 38.3 testing requirements, IATA and ICAO air transport standards, state-of-charge limitations, short-circuit prevention measures, and UN-certified packaging specifications. These requirements increase operational complexity and create additional value-added service opportunities for logistics providers.

Storage presents another significant challenge. Batteries require dedicated handling procedures and cannot be stored alongside certain hazardous materials. Temperature-controlled and ventilated facilities are increasingly becoming essential, with optimal storage conditions typically maintained between 20°C and 25°C to preserve battery performance and minimize safety risks.

As battery trade volumes continue to grow, ports, distribution centers, and warehouses are investing in specialized battery handling infrastructure to support evolving market requirements.

Is Compliance Now the Biggest Cost in Battery Logistics?

One of the most notable characteristics of lithium-ion battery logistics is that transportation economics are increasingly driven by compliance rather than freight movement itself.

Analysis of battery shipments from China to Europe shows that sea freight remains the most economical option for large-volume battery transportation, with base freight rates ranging between USD 1–3 per kilogram compared to USD 8–15 per kilogram for air freight.

However, dangerous goods (DG) surcharges significantly alter the overall cost structure. Additional expenses related to hazardous goods handling, insurance, documentation, and regulatory compliance often account for a substantial portion of total logistics expenditure.

For large-scale battery shipments, DG surcharges alone can add 30% to 50% or more on top of the base freight rate, with insurance and documentation requirements compounding the effect further. This trend highlights how battery logistics has evolved into a compliance-intensive business where safety management capabilities directly influence profitability and competitiveness.

Regional Trade Patterns Reflect China’s Export Leadership

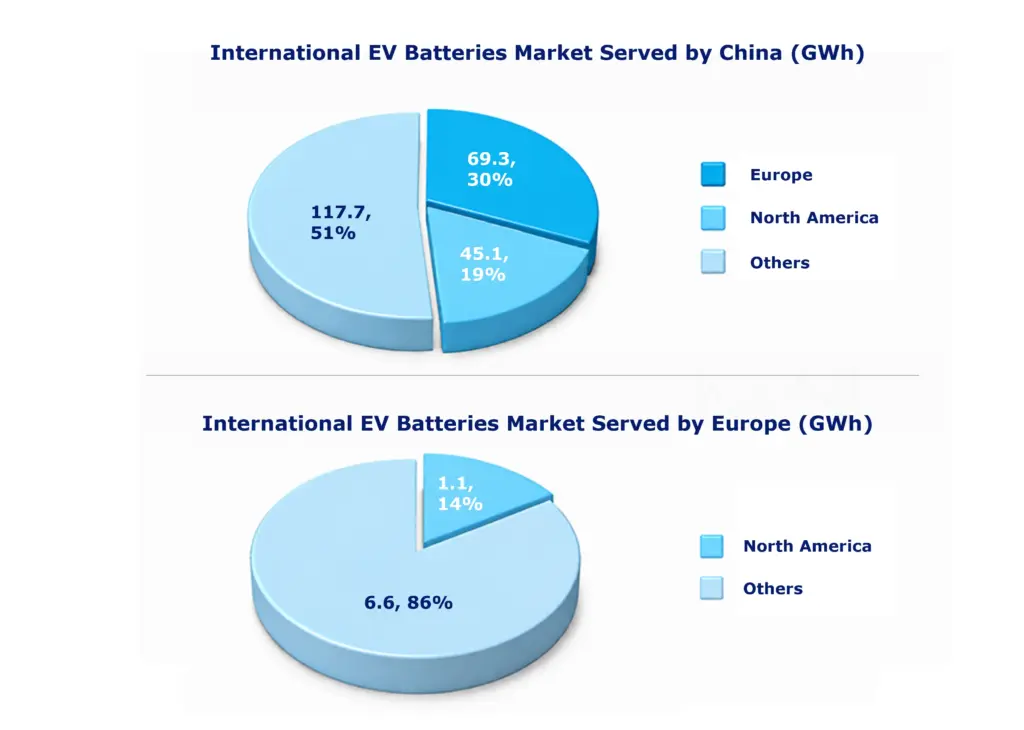

Global EV battery trade flows remain heavily concentrated around China, reinforcing its position as the world’s primary battery manufacturing hub.

China serves a broad international market, with approximately 117.7 GWh (51%) of exported EV battery capacity directed toward other global markets, 69.3 GWh (30%) supplied to Europe, and 45.1 GWh (19%) shipped to North America. This highlights China’s critical role in supporting EV production beyond its domestic market and underscores the importance of Asia-Europe and Asia-North America battery trade corridors.

In contrast, Europe’s battery exports remain comparatively limited and geographically concentrated. Of the EV battery capacity supplied by Europe to international markets, approximately 6.6 GWh (86%) is directed toward other regions, while only 1.1 GWh (14%) is exported to North America.

The trade distribution illustrates a significant imbalance in global battery supply chains. While Europe and North America continue to invest in local gigafactory capacity, international EV battery markets remain heavily dependent on Chinese production. Consequently, logistics providers with capabilities in long-distance hazardous goods transportation, international compliance management, and cross-border battery handling are likely to benefit from sustained growth in these major battery trade lanes.

The Next Frontier: Battery Circularity and Reverse Logistics

Beyond forward supply chains, the emergence of the battery circular economy is creating an entirely new logistics segment.

Governments worldwide are introducing regulations to promote battery reuse, refurbishment, second-life applications, and recycling. These initiatives require sophisticated reverse logistics networks capable of safely transporting end-of-life batteries for material recovery and processing.

China’s battery recycling regulations, updated in 2024, mandate high recovery rates for critical materials, including a lithium recovery requirement raised to 90%, up from 85% previously. Similarly, the European Union’s Critical Raw Materials Act aims to source at least 25% of critical mineral consumption from domestic recycling by 2030.

As European battery recycling capacity is expected to reach roughly 500,000 tonnes annually by 2030, reverse logistics networks will become increasingly important components of the broader battery value chain.

Outlook

The future of battery logistics extends far beyond transportation. Growing battery demand, concentrated manufacturing hubs, expanding global trade routes, stricter safety regulations, and the rise of battery recycling are collectively transforming logistics into a strategic growth market.

Organizations that invest early in specialized transportation capabilities, compliant warehousing infrastructure, digital tracking systems, and reverse logistics networks will be best positioned to capitalize on one of the fastest-growing segments of the global energy transition.

As electrification accelerates worldwide, the companies that move, store, recover, and manage batteries safely and efficiently will play an increasingly critical role in enabling the next phase of global energy transformation.

Let’s talk strategy. Our experts are ready to help you turn these shifts into a competitive edge. Reach out at contact@iebrain.com.