Europe’s automotive industry has entered one of its most strategically important industrial transitions in decades. With accelerating electrification and EV adoption in major markets, battery manufacturing is becoming a vital aspect of automotive competitiveness, industrial resilience, and long-term technological leadership.

For years, Europe has been one of the leading regional EV markets due to stringent EU emission regulations. However, battery manufacturing remained concentrated in Asia, particularly China, South Korea, and Japan. But now, the dynamic is changing. Governments, automotive OEMs, and battery producers are aggressively investing in localized battery production, gigafactories development, access to raw materials, and integration into the battery value chain to reduce supply chain vulnerabilities and strengthen Europe’s position in the global EV ecosystem.

However, this transition to battery production is occurring in a highly competitive and interdependent global environment. In addition to Chinese battery producers expanding their presence throughout the region, OEMs are reshaping sourcing and chemistry strategies. Moreover, the industry is transitioning towards a more differentiated battery ecosystem with both NMC and LFP chemistries anticipated to coexist.

This transition is no longer only about scaling battery production capacity; it is increasingly about determining who controls battery technology, manufacturing expertise, supply chains, and the broader economics of electrified mobility.

How is Europe’s battery manufacturing ecosystem evolving?

Europe is transforming from an EV consumption market into a rapidly-growing battery production hub. Over the last few years, Europe has seen a significant rise in announced giga-factory projects, strategic investments, and localization initiatives designed to build a reliable battery ecosystem capable of sustaining long-term EV growth.

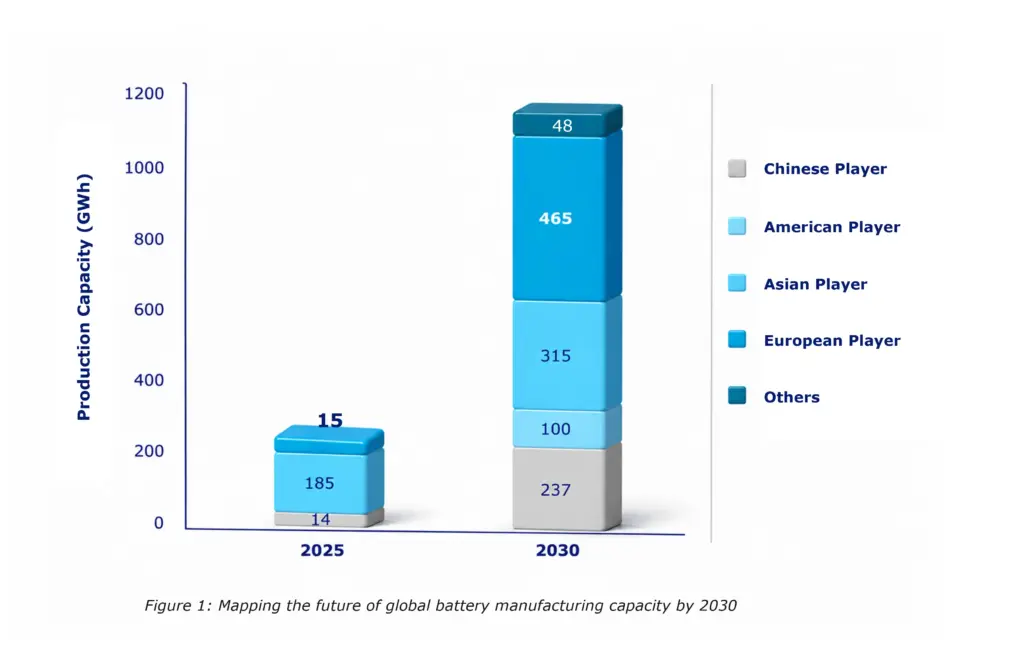

According to secondary research sources, Europe’s lithium-ion battery production capacity may grow from approximately 15 GWh in 2025 to over 465 GWh by 2030. This growth will likely occur as a result of European OEM investments, government support of localized production, and increasing participation from Asian battery manufacturers.

An important characteristic of this transition is the amount of announced manufacturing projects taking place across Europe. Countries like Germany, Hungary, France, Spain, Poland, and Sweden are emerging as the top locations for battery manufacture because they possess established automotive bases; offer financial incentives; and are located near existing OEM production centers.

Global Battery Manufacturing Capacity Substantial Expansion (2025-2030)

Among them, Hungary is becoming popular as a strategic hotspot for battery manufacturing. The country’s authorities have attracted significant investments from Asian battery companies to establish local manufacturing operations for several reasons. These include Hungary’s established automotive base; favorable industrial policy; and its geographical advantages within Europe.

Among them, Hungary is becoming popular as a strategic hotspot for battery manufacturing. The country’s authorities have attracted significant investments from Asian battery companies to establish local manufacturing operations for several reasons. These include Hungary’s established automotive base; favorable industrial policy; and its geographical advantages within Europe.

In addition to these factors, Chinese battery manufacturers like CATL, CALB, EVE Energy, and Sunwoda are expanding their locally manufactured product lines across Europe. Meanwhile, European battery initiatives, such as Volkswagen’s PowerCo, are contributing to the development of the overall scale of battery manufacturing in the region.

While there is clearly an increasing trend toward localizing battery production, Europe’s development of battery production is still dependent upon foreign technology and manufacturing expertise. Many Asian battery companies continue to play a central role in Europe’s development efforts by establishing local production facilities, engaging in technology partnership agreements, and providing operational know-how.

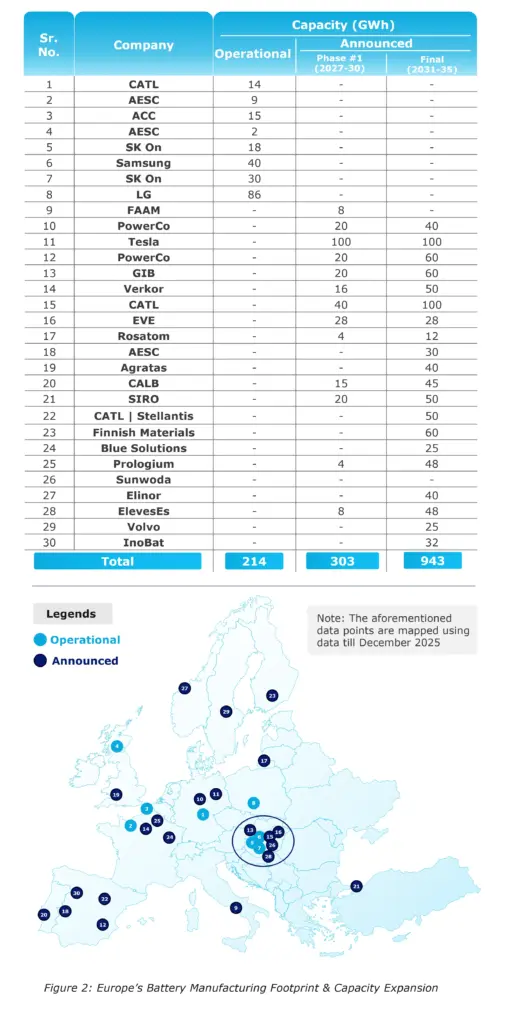

Assessment of Battery Cell Footprints Across Europe

**Note: The aforementioned data points are mapped using data till December 2025

This represents an unusual industrial dynamic. On one side, Europe is working to improve its ability to produce domestically. On the other hand, it is concurrently leveraging foreign expertise to efficiently develop its manufacturing capabilities on a large scale and remain competitively positioned internationally.

However, there are significant risks associated with realizing these objectives. A large proportion of Europe’s projected battery capacity will rely on announced or early-stage projects versus completed facilities. Therefore, financing challenges; permitting processes; energy costs; labor shortages; and difficulties accessing raw materials can negatively impact execution.

Therefore, in such scenarios, Europe’s battery transition should not be viewed as having secured industrial dominance, but rather as an ongoing scaling phase for Europe’s industrial sectors. Execution capability will ultimately determine whether Europe will retain its competitive advantage in this sector.

Why is the battery chemistry transition becoming strategically important?

Europe’s battery ecosystem is evolving from an NMC-dominated marketplace toward a dual-chemistry model where both chemistries provide alternative solutions for different vehicle types; price segments; and performance characteristics. NMC (Nickel Manganese Cobalt) batteries currently represent the majority of Europe’s EV landscape, particularly for high-end and long-range electric vehicles—because they provide greater energy density than LFP batteries. Therefore, they provide better options when performance, vehicle efficiency, and driving range become critical differentiating features.

Meanwhile, LFP (Lithium Iron Phosphate) batteries are quickly becoming preferred for low-cost electric vehicle segments and urban mobility applications. Their lower cost structures compared to NMC batteries; enhanced thermal stability; and diminished reliance on scarce raw materials make them increasingly appealing alternatives for low-cost vehicle platforms.

This shift reflects a broader market segmentation strategy rather than a direct chemistry replacement cycle.

To fortify, Volkswagen is planning to incorporate LFP in conjunction with continuing its NMC strategy for high-performance EV models. Renault is similarly planning to adopt LFP for some future electric vehicle models focused on affordability, while Ford plans to invest in LFP manufacturing capacity within Europe while maintaining its NMC distribution across multiple EV models.

Similarly, Stellantis is planning to strengthen its LFP ecosystem through partnerships and localized production initiatives. Tesla continues to utilize a dual-chemistry strategy by deploying both NMC and LFP batteries across different vehicle models and regional markets. Hyundai is selecting chemistry based on performance requirements as well as vehicle positioning.

Also, NMC chemistry remains strategically important because premium EV positioning, long-range requirements, and higher-performance applications continue to favor higher energy-density solutions.

As a result, Europe’s battery ecosystem will evolve toward a multi-chemistry ecosystem where vehicle selection becomes increasingly aligned with vehicle design; consumer use patterns; and pricing strategies.

The long-term implication is significant. Battery chemistry is no longer simply a technical decision; it is becoming a strategic lever that influences vehicle affordability, supply-chain resilience, manufacturing economics, and competitive differentiation.

How are OEMs expanding control across the battery value chain?

Europe’s automotive OEMs are increasingly moving beyond vehicle manufacturing and expanding deeper into the battery value chain. Rather than relying solely on external suppliers, companies are building capabilities across battery materials, cell manufacturing, pack assembly, recycling, refining, and repair infrastructure.

This reflects a broader realization that battery control is becoming a long-term competitive moat rather than merely a procurement function.

Leading OEMs including Volkswagen, BMW, Mercedes-Benz, Renault, and Stellantis are actively pursuing vertical integration strategies aimed at securing supply stability, improving operational control, and reducing long-term cost volatility.

Volkswagen Group remains the most vertically integrated player in the group. Through its PowerCo joint venture and partnerships with Umicore, the group has secured coverage across every stage — from precursor cathode active material (pCAM) through to refining and recycling. With over 1.1 million EVs sold in 2024 and an end-of-life battery feedstock estimate of 5,291 tonnes, VW has both the scale and the infrastructure to close the battery loop internally.

BMW Group, despite generating the largest EoL feedstock volume at 5,467 tonnes, shows a more fragmented picture. Cell and pack production are in-house, recycling capabilities are established, but repair and CAM remain gaps — with partnerships filling the middle. That asymmetry between feedstock scale and chain completeness is worth watching.

BMW Group, despite generating the largest EoL feedstock volume at 5,467 tonnes, shows a more fragmented picture. Cell and pack production are in-house, recycling capabilities are established, but repair and CAM remain gaps — with partnerships filling the middle. That asymmetry between feedstock scale and chain completeness is worth watching.

At 22% year-on-year EV sales growth — the fastest among the four — Mercedes-Benz is scaling rapidly, but its battery value chain is still catching up. Upstream capabilities in pCAM and CAM are currently absent or handled through partnerships, and repair infrastructure isn’t expected until 2026. For a brand that commands premium margins, closing those gaps will be critical as battery costs increasingly determine vehicle economics.

Stellantis presents the most partnership-dependent model. Its EoL feedstock estimate of 1,389 tonnes — by far the lowest — reflects a smaller EV footprint relative to its peers. With no in-house pCAM capability and a heavy reliance on joint ventures and third-party arrangements for recycling and pre-treatment, the question is whether this is a deliberate asset-light strategy or a gap that needs closing as volumes grow.

The growing emphasis on recycling and circularity is particularly important. As EV adoption scales, OEMs are recognizing that battery recycling will become essential not only for sustainability compliance, but also for recovering critical materials such as lithium, nickel, cobalt, and manganese.

Several interconnected factors are driving this vertical integration trend.

Cost optimization: Battery costs remain one of the largest contributors to EV pricing. Greater control across the value chain enables OEMs to improve margins and reduce long-term procurement volatility.

Supply security: Global supply-chain disruptions and geopolitical tensions have exposed vulnerabilities in battery sourcing. Vertical integration allows OEMs to secure more stable access to materials and manufacturing capacity.

Raw material access: Competition for critical minerals is intensifying globally. OEMs are increasingly seeking direct involvement in material sourcing and refining to reduce dependency risks.

Geopolitical uncertainty: Battery manufacturing is becoming deeply connected to industrial policy, trade dynamics, and strategic autonomy considerations, particularly within Europe.

Sustainability regulations: European sustainability regulations and carbon reduction targets are pushing OEMs toward localized, traceable, and circular battery ecosystems.

The broader implication is clear: battery manufacturing is evolving into a strategically integrated industrial ecosystem where control over materials, chemistry, production, and recycling may ultimately determine automotive competitiveness in the EV era.

Can Europe reduce dependence on Chinese battery players?

Europe’s battery manufacturing ambitions are strongly tied to localization, but Chinese battery companies remain deeply embedded within the region’s evolving battery ecosystem.

While Europe is investing heavily in domestic production capabilities, Chinese manufacturers continue expanding their footprint through giga-factory investments, technology partnerships, and joint ventures with European OEMs.

Current estimates suggest that Chinese players account for roughly 6.5% of Europe’s battery manufacturing capacity today, with their share potentially rising toward 20% by 2030 as additional projects and collaborations move forward.

CATL has emerged as one of the most influential players within Europe’s battery ecosystem through large-scale investments and strategic partnerships with automotive OEMs. Companies including CALB, EVE Energy, and Sunwoda are similarly leveraging their manufacturing scale, process expertise, and battery technology capabilities to strengthen their long-term position within the European market.

At the same time, European OEMs continue relying on Chinese expertise for battery technology, manufacturing efficiency, and large-scale industrial execution.

This creates an important strategic nuance: Europe’s battery ecosystem is not fully decoupling from China. Instead, it is selectively integrating Chinese participation while simultaneously attempting to strengthen local industrial resilience.

Partnerships increasingly reflect this balancing strategy. Stellantis and CATL, for example, are collaborating on localized LFP battery manufacturing initiatives within Europe, while several European battery projects continue depending on Asian process expertise and technology transfer.

This interconnected landscape highlights the growing tension between industrial sovereignty and competitive necessity.

On one hand, Europe aims to reduce overdependence on external supply chains and strengthen domestic battery production capabilities. On the other hand, Chinese companies currently possess substantial advantages in manufacturing scale, cost competitiveness, raw material processing, and battery technology maturity.

As a result, Europe’s strategy appears to be evolving toward controlled integration rather than outright separation.

The long-term challenge for Europe will be determining how to balance localization ambitions with the economic realities of global battery manufacturing competitiveness.

Future Outlook: Europe’s battery ecosystem in a decisive phase

Europe’s battery manufacturing ecosystem is moving beyond its early developmental stage and entering a critical industrial scaling phase. Over the next decade, battery production capacity, chemistry diversification, value-chain integration, and manufacturing execution will increasingly shape the competitiveness of the European automotive industry.

Several structural trends are expected to define this next phase.

First, battery manufacturing will become central to automotive competitiveness rather than functioning as a supporting supply-chain activity. OEMs that secure stronger control over battery technologies, materials, and manufacturing ecosystems are likely to gain long-term advantages in cost structure, resilience, and product differentiation.

Second, Europe’s battery chemistry landscape is expected to remain diversified. NMC batteries will likely continue dominating premium and long-range vehicle segments, while LFP adoption expands across affordable and urban-focused EV categories. This dual-chemistry ecosystem will shape future sourcing, manufacturing, and product strategies.

Third, vertical integration is expected to accelerate further as OEMs seek tighter control over raw materials, recycling, refining, and battery manufacturing infrastructure. Closed-loop battery ecosystems may eventually become a defining competitive advantage across the EV industry.

At the same time, Chinese battery manufacturers are expected to remain strategically influential within Europe despite localization efforts. Their manufacturing expertise, technology leadership, and established supply-chain capabilities will likely continue playing an important role in Europe’s battery industrialization journey.

However, the next major challenge will not simply be announcing projects or securing investments. It will be execution at scale.

Europe’s ability to convert announced giga-factory pipelines into commercially viable, cost-competitive, and technologically advanced manufacturing ecosystems will ultimately determine whether the region can establish long-term leadership within the global battery industry.

Looking to understand the strategic implications of Europe’s evolving battery ecosystem? Reach out to our industry experts by filling out the form below or contacting us at contact@iebrain.com.