Digital transformation of the Indian energy sector is moving from pilots to scaled execution, but the opportunity remains uneven across digital layers, infrastructure readiness, and product ownership.

Overview

India’s energy sector is undergoing a digital transformation in energy, yet this is still a “work-in-progress” rather than an accomplished transformation. The pace of this transition is influenced by various factors, including policy support for digitalization, increased public-private partnerships, rapidly increasing smart infrastructure and increasing complexity within grids due to increased amounts of renewables. At the same time, there remain some of the traditional issues associated with the energy sector including fragmented systems, non-standardized data formats and varying degrees of preparedness among utilities.

What makes the shift important is not only technology adoption, but the attempt to build a more connected operating model. Digital tools have been increasingly utilized throughout the entire value chain of the power sector to increase visibility, streamline operations, and enable better decision-making. This digital transformation in energy will ultimately depend on how effectively India aligns policy ambitions with execution capability and long-term investment strategies.

Major Developments & Growth Indicators in India’s Energy Sector

Several developments point to a broader push toward digitalizing India’s energy ecosystem. Examples of advancements that demonstrate a unified approach to creating a digital foundation for the power sector include smart metering, grid digitization; analytical based operational processes; and digital platforms used to monitor & control all elements of the system.

Policy support

India’s digital energy push is being shaped by a mix of policy, infrastructure, and collaboration. The Ministry of Power has introduced the India Energy Stack (IES) as a Digital Public Infrastructure, with execution planned toward FY 2026-27, while the Smart Meter National Programme continues to support smart meter adoption through EESL and DISCOMs.

The policy layer is also expanding through the National Smart Grid Mission, which supports broader grid modernization, and through state-led efforts such as the Urja Sanvardhanam Platform in Gujarat and the Maharashtra collaboration between Maharashtra State Electricity Distribution Company Limited (MSEDCL) and Global Energy Alliance for People and Planet (GEAPP).

Funding & Incentivization

Funding and incentives are adding momentum. A 100% waiver of Inter-State Transmission Charges for energy storage systems remains available until June 2028, which can support storage-linked digital grid planning. The Indo-US Joint Clean Energy Research and Development Centre is funding R&D projects that improve grid reliability, flexibility, and efficiency. In addition, the Revamped Distribution Sector Scheme has sanctioned around Rs 20.33 crore for smart meters and data systems.

Key Players Driving Strategic Investments in India’s Smart Grid Ecosystem

India’s smart grid transformation is being propelled by a combination of domestic innovators, global technology leaders, and international development organizations. While Indian companies are strengthening digital utility capabilities through AI-enabled platforms and smart metering, global firms are investing in advanced grid infrastructure, digitalization, and clean energy technologies. Complementing these efforts, multilateral collaborations are providing financial, technical, and policy support to accelerate nationwide grid modernization.

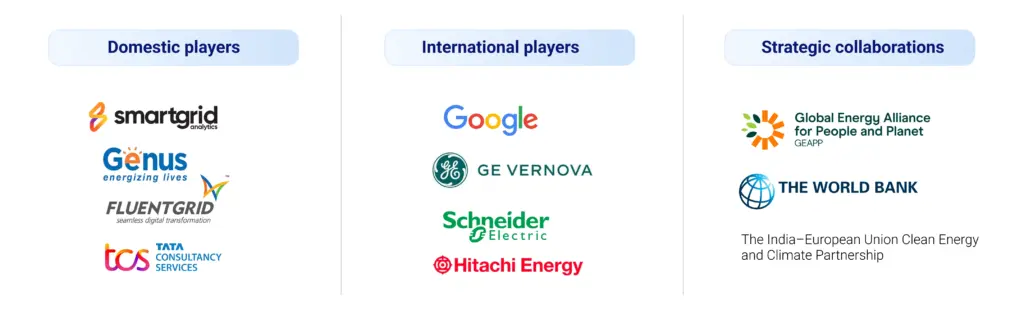

Domestic Players Strengthening Digital Grid Infrastructure

Indian technology companies are increasingly investing in intelligent grid solutions to support utilities in their digital transformation journey.

- Smart Grid Analytics secured USD 3.3 million in funding to expand its AI-powered grid and energy management platform, highlighting growing investor confidence in AI-driven utility solutions.

- Genus Power Infrastructures has emerged as a leading player in India’s smart metering ecosystem, attracting significant private equity investment of approximately INR 519 crore to strengthen manufacturing capacity and market expansion.

- Fluentgrid continues to invest in expanding its digital utility platform, enabling utilities to build integrated digital ecosystems for improved grid operations and customer management.

- Tata Consultancy Services (TCS) is making substantial investments of around USD 6–7 billion across utility digital platforms, with a strong emphasis on AI-enabled energy management, smart grid modernization, and intelligent utility operations.

International Players Expanding India’s Smart Grid Landscape

Global technology companies are making strategic investments that reinforce India’s ambition to build a digitally connected, resilient, and sustainable power infrastructure.

- Google announced a USD 15 billion investment to establish AI-focused data centre infrastructure in India, supporting the computational backbone required for next-generation digital energy applications.

- GE Vernova is investing approximately USD 16 million to strengthen smart grid infrastructure across multiple Indian cities by 2027, contributing to advanced grid reliability and automation.

- Schneider Electric continues to expand its investments in India’s smart grid and digital energy sector by enhancing manufacturing capabilities for AI-enabled, IoT-driven, and sustainable energy technologies.

- Hitachi Energy plans to invest around USD 250 million to strengthen smart grid capabilities, supporting grid resilience, transmission efficiency, and digital power infrastructure across the country.

International Collaborations Accelerating Grid Modernization

Beyond corporate investments, strategic partnerships with international institutions are playing a pivotal role in advancing India’s smart grid ecosystem through funding, technology transfer, and policy support.

- The Global Energy Alliance for People and Planet (GEAPP) is supporting the development of digital twins for Rajasthan’s electricity distribution network while contributing to grid modernization initiatives in Maharashtra.

- The World Bank continues to provide financial and technical assistance through programs focused on enhancing electricity distribution, improving grid reliability, expanding energy access, and accelerating digitalization.

- The India–European Union Clean Energy and Climate Partnership is fostering collaboration on clean energy technologies, sustainable grid development, and climate-focused energy transition initiatives.

Collectively, these investments demonstrate that India’s smart grid ecosystem is evolving through a multi-stakeholder approach, where domestic innovation, international capital, and cross-border partnerships are converging to build a more intelligent, resilient, and digitally enabled power network.

India Energy Stack: Building the Digital Backbone of the Future Energy Ecosystem

The India Energy Stack (IES) is one of the most important structural moves in the sector’s digital journey. It provides a unified digital foundation to improve traceability, interoperability, transparency, and service delivery across energy stakeholders. By introducing common identifiers, open APIs, and consent-based data sharing, it aims to reduce friction between consumers, utilities, policymakers, and technology providers.

The logic behind IES is practical rather than aspirational. It seeks to modernize the power sector through a common digital language, helping utilities manage assets and transactions more efficiently while giving consumers better visibility and choice. The Utility Intelligence Platform, built on top of IES, adds a decision-support layer for DISCOMs, policymakers, and consumers. If implemented consistently, IES could become a useful enabler of standardization, but its impact will depend on adoption depth and integration quality.

The Evolution of AI, Digitalization & Robotics Across India’s Energy Landscape

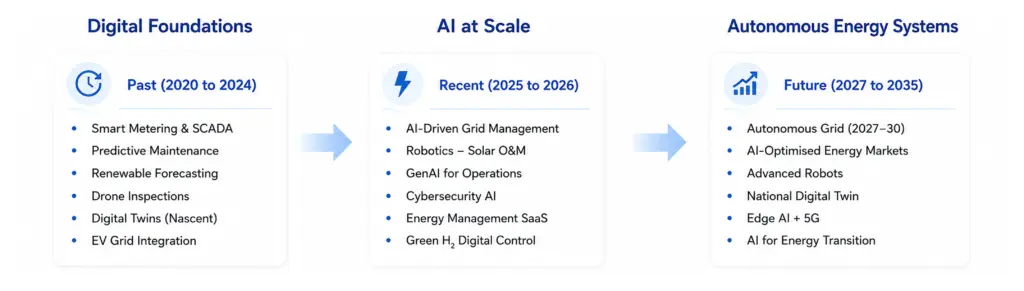

The sector’s technology adoption has moved through distinct phases. Between 2020 and 2024, India saw the expansion of smart meters and SCADA-based distribution management systems, along with early use cases in predictive maintenance, renewable forecasting, drone inspections, digital twins, and EV grid integration. These applications showed that digital tools could address both operational visibility and asset performance, even if many deployments were still partial or nascent.

The 2025-26 period reflects a more mature phase of adoption. AI-driven grid management is now being used by NLDC and SLDCs for load forecasting and congestion management, while utility-scale solar operators are deploying robotic panel-cleaning systems. In the upstream and downstream energy segments, companies such as ONGC and Reliance are using GenAI for document intelligence, well log analysis, and HSE reporting. AI-based cybersecurity tools are also being deployed to strengthen OT/IT threat detection, and Indian startups are expanding AI-powered energy management SaaS offerings for commercial and industrial users. Green hydrogen projects are also beginning to use digital process control for electrolyzer operations.

The future pipeline is more ambitious, but it should be read as a direction of travel rather than a certainty. From 2027 to 2035, the sector could move toward autonomous, self-healing distribution grids, AI-optimized energy markets, national digital twins, and stronger edge AI deployment through 5G-enabled infrastructure. Robotics may also become more important in hazardous environments, while AI-driven tools may support carbon accounting, battery analytics, and green hydrogen cost optimization. These are plausible next steps, but their speed will depend on scale, policy continuity, and economics.

Building India’s Energy-Tech Advantage: Strengths Today, Opportunities Tomorrow

India has a strong foundation to build a competitive energy-tech ecosystem. Its advantages include deep IT talent, relatively cost-effective AI development, and large public sector anchor clients that can accelerate adoption. This gives the country an advantage in software, analytics, and digital platforms, especially where scale and affordability matter.

The main gap is in indigenous robotics & hardware. Software capabilities are scaling faster than the underlying physical technologies needed for advanced automation, inspection, and field operations. That imbalance does not weaken the digital opportunity, but it does show where ecosystem development still needs to deepen. If India can close this hardware and robotics gap, the digital energy stack will become more complete and more resilient.

Closing Perspective

Overall, India’s digital transformation in the energy sector is real, measurable, and increasingly visible across policy, operations, and technology deployment. The direction is encouraging, but the sector is still balancing ambition with execution. The strongest gains so far are in data visibility, smart infrastructure, and AI-assisted operations, while the next phase will depend on interoperability, scaling discipline, and stronger hardware capabilities.

Looking to navigate the next wave of digital transformation in energy? Reach out to our cross-domain experts (contact@iebrain.com) to explore strategic opportunities across technology adoption, digital infrastructure, market intelligence, investment strategy, regulatory landscape, and business growth; helping you build future-ready solutions with confidence.